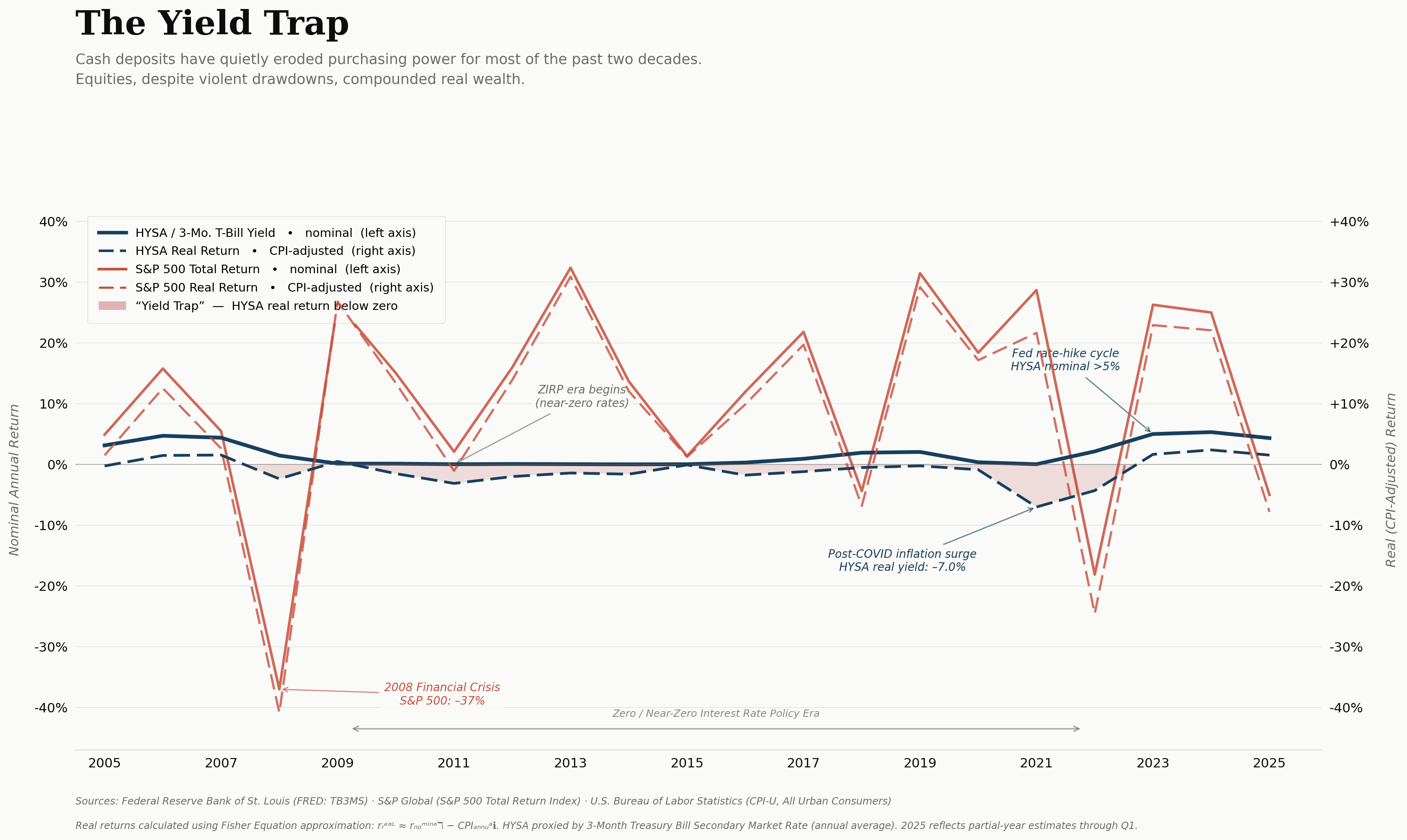

For the better part of a decade, the choice between a savings account and the stock market was a binary one. With interest rates pinned near zero by the Federal Reserve, cash was "trash"—a depreciating asset that served only as a psychological safety net for the ultra-conservative. But as the central bank’s aggressive campaign against inflation pushed yields to levels not seen in fifteen years, the calculus changed. Today, the High-Yield Savings Account (HYSA) is no longer a dormant parking spot; it is a legitimate competitor for capital.

Yet, as investors flock to the 4% and 5% guaranteed returns of online banks, a dangerous comparison has emerged. Retail investors are increasingly weighing these "risk-free" cash yields against broad-market ETFs like the Vanguard S&P 500 (VOO) or the SPDR S&P 500 (SPY). On the surface, the choice seems simple: take the guaranteed 4.5% or chase a historical 10% with a chance of a 20% drawdown. In reality, this is not a choice between two similar products; it is a choice between two entirely different financial dimensions.

The Psychology of the 'Nominal' Win

The allure of the HYSA lies in its linearity. Every month, the balance goes up. There are no red days, no market "corrections," and no volatility-induced insomnia. For many, this is the definition of safety. In the professional world, however, we distinguish between nominal safety and real safety.

A HYSA provides nominal safety—you will not lose your principal. But it offers very little protection against inflation. When inflation sits at 3% and your HYSA pays 4.5%, your real "wealth-building" rate is a meager 1.5%. After accounting for taxes (which are levied at ordinary income rates), that real return often vanishes entirely. In contrast, equities like VOO or SPY are ownership stakes in companies that have the power to raise prices, providing a natural, albeit volatile, hedge against the rising cost of living.

VOO and SPY: The Safe Haven Misnomer

It has become a common refrain in personal finance circles that the S&P 500 is "safe." This is a half-truth that requires careful parsing. Over a 20-year horizon, the S&P 500 has never yielded a negative return. In that context, it is arguably the safest wealth-building engine in history. But over a 12-month horizon, the S&P 500 is a casino where the house has only a slight edge.

The mistake many investors make is using VOO or SPY for "short-term safety." If you need your capital for a house down payment in eighteen months, a broad-market ETF is a reckless gamble, not a safe investment. Conversely, if your goal is retirement in two decades, holding significant sums in an HYSA is a form of "slow-motion risk." You aren't losing money to the market; you are losing the future value of that money to the power of compounding equity growth.

The Invisible Drag: Taxes and Efficiency

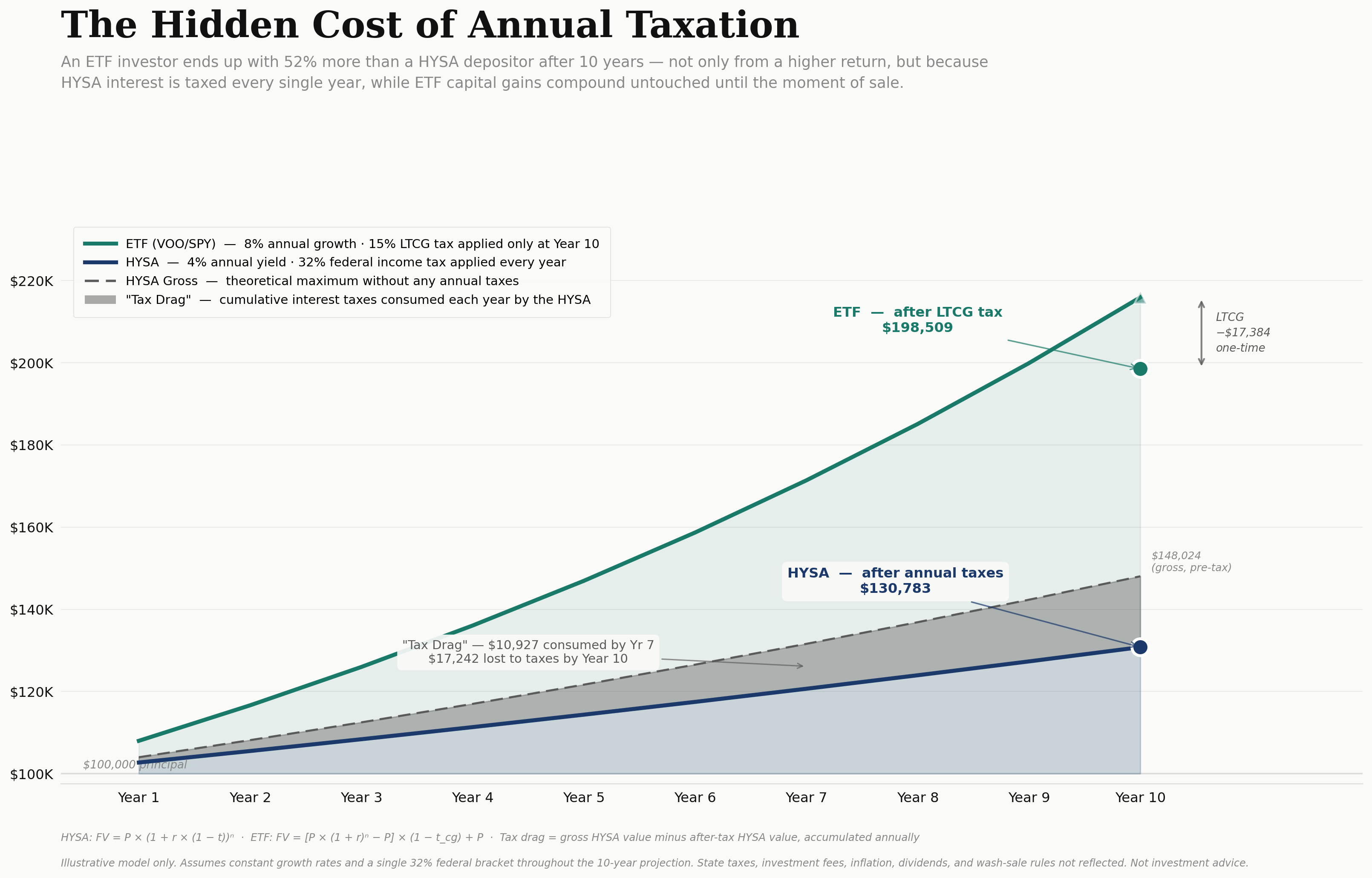

One of the most overlooked aspects of this comparison is the tax man’s cut. Interest from a HYSA is taxed as ordinary income—the same rate as your salary. For a high-earner, this can mean losing nearly 40-50% of that "guaranteed" yield before the money even hits their spending account.

ETFs like VOO and SPY are vastly more tax-efficient. They primarily generate wealth through capital appreciation. You only pay taxes when you sell, allowing your money to compound on a pre-tax basis for years. Furthermore, when you do sell, you are often taxed at the long-term capital gains rate, which is significantly lower than ordinary income brackets. For the serious builder of wealth, the "guaranteed" return of a HYSA often looks significantly less attractive once the 1099-INT arrives in January.

The Duration Mismatch and Reinvestment Risk

When you put money in a HYSA, you are effectively a lender. You are lending your cash to the bank, and they are paying you a floating rate. That rate can—and will—drop the moment the Federal Reserve signals a pivot. This is known as "reinvestment risk." You might enjoy 5% today, but you have no guarantee of 5% tomorrow. If rates drop to 2%, your income stream is slashed by 60% overnight.

When you buy VOO or SPY, you are an owner. You own the future cash flows of the 500 most profitable companies in the United States. While those cash flows fluctuate, the long-term trajectory of American corporate earnings has historically been upward. You are not just capturing a rate; you are capturing productivity and innovation. While the "owner" suffers through volatility, they are rewarded with a premium that the "lender" can never achieve.

Strategy: The 'Two-Pocket' Rule

To navigate this, investors should stop viewing these as competing assets and start viewing them as complementary tools.

- Pocket 1 (The HYSA): Reserve this for your Emergency Fund and known liabilities within the next 24 months. This is your "Operations" capital. It should be sized to cover 3–6 months of living expenses and any upcoming large purchases (taxes, down payments, tuition).

- Pocket 2 (VOO/SPY): This is your "Growth" capital. If the time horizon is longer than five years, the historical volatility of the S&P 500 is simply the "entry fee" for the premium return over cash.

Conclusion: Solving for the Right Variable

The debate between HYSA and S&P 500 ETFs isn't about which is "better"—it's about which matches your timeline. A HYSA is a tool for preservation; VOO and SPY are tools for creation.

In a high-rate environment, the "yield trap" is the temptation to stay in cash far longer than necessary because it feels comfortable. But comfort is rarely the companion of significant wealth. For the investor looking to build a legacy, the volatility of the stock market is not a bug; it is the feature that allows for long-term outperformance. The safest move you can make is knowing exactly which tool you are holding, and why.